How Credit Actually Works (And Why It Matters More Than You Think)

You go to rent your first apartment and the application asks for your credit history. You apply for a car loan and suddenly your score determines whether you pay $400 a month or $500. You're trying to land a job and find out the employer runs a credit check as part of the background screen.

Credit shows up everywhere, usually when you need it most. But a lot of people don't fully understand how credit works, what's actually in a credit score, or how to start if they're at zero.

Here's a quick breakdown of how it all works.

How credit works, in plain English

Credit is the ability to borrow money with the promise to pay it back later. When you use a credit card, take out a loan, or even sign up for a phone plan that bills you at the end of the month, someone is extending you credit. They're trusting that you'll hold up your end.

Good credit means you've kept those promises. You've paid on time, managed balances responsibly, and shown a reliable pattern. The more of that history you have, the more lenders are willing to trust you, and the better terms you get when they do.

A history of missed or late payments sends the opposite signal. It makes future credit harder to get, more expensive when you do get it, and slower to rebuild.

How lenders actually decide

When a lender is considering whether to extend credit, they look at three things:

Credit history is the full record of everything you've ever borrowed. Every credit card, loan, or line of credit you've opened or closed. How much you owe. Whether you've paid on time. It's the raw story.

Credit report is the document that pulls that history together. It includes your accounts, payment history, personal info, and any recent inquiries. Your report is generated by one of three major credit bureaus: Equifax, TransUnion, and Experian. Lenders use it to decide whether to extend credit to you, and on what terms.

Credit score is the three-digit number (usually 300–850) that summarizes everything above. Think of it like a grade. Higher is better. A score in the high 700s will get you meaningfully better interest rates than a score in the low 600s. A score below 600 can be the difference between getting approved and getting denied.

Inquiries come in two flavors. Soft inquiries, like checking your own credit or pre-approval offers, don't affect your score. Hard inquiries happen when a lender actually pulls your credit after you apply for something, and they can ding your score a few points and stick around on your report for up to two years. A couple here and there won't wreck you. Five in one month will.

What goes into your score

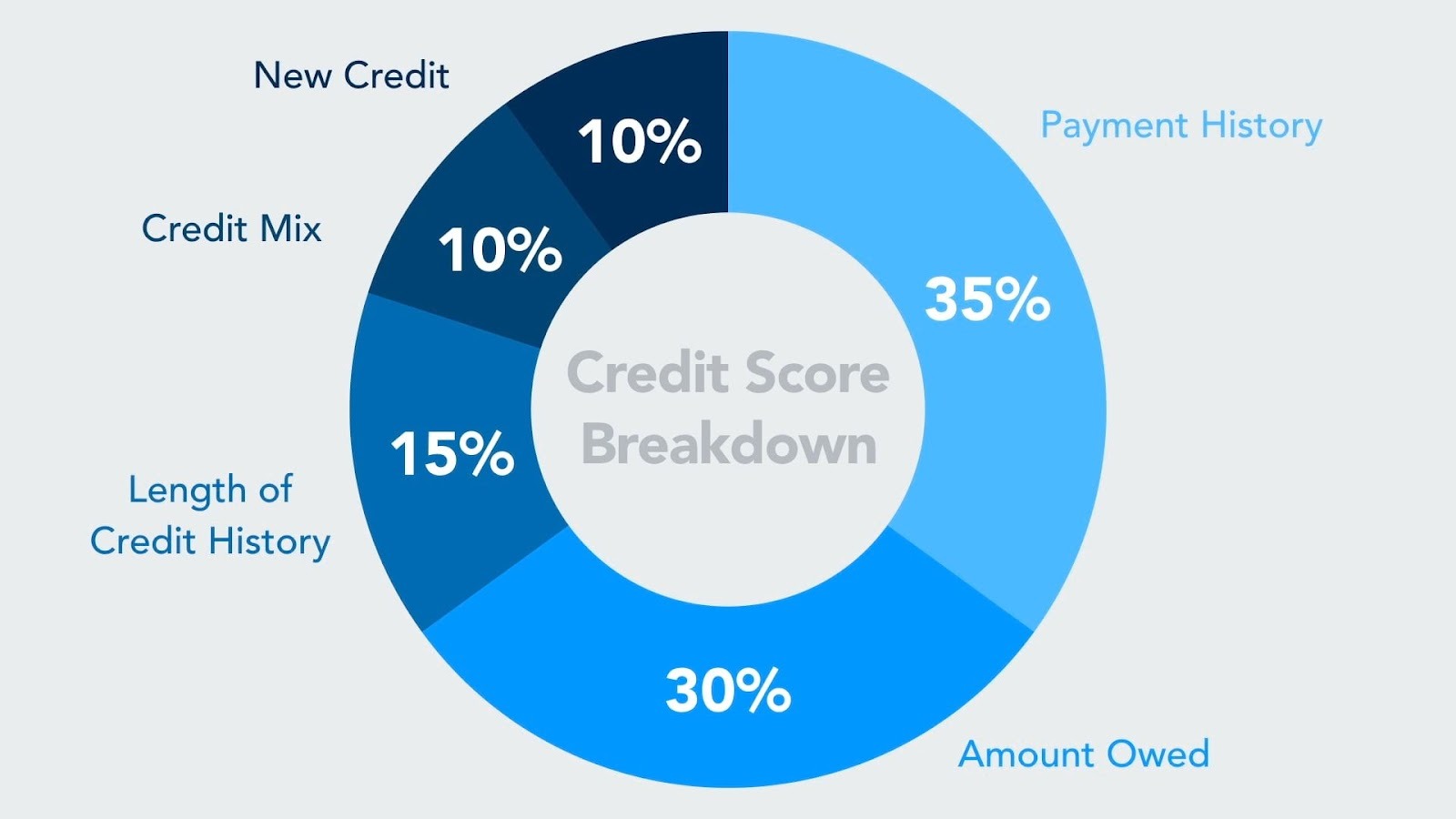

Your credit score isn't some mysterious formula. FICO, the company that creates the most widely used credit score, breaks it down into five categories:

- Payment history (35%). Whether you pay on time. This is the biggest factor by a wide margin.

- Amounts owed (30%). How much of your available credit you're using. Lower utilization is better. Maxing out your cards hurts, even if you pay them off in full.

- Length of credit history (15%). How long you've had credit accounts open. Older is better, which is why starting early matters.

- New credit (10%). How often you're applying for new credit. Too many applications in a short window signals risk.

- Credit mix (10%). Whether you have different types of credit, like cards and loans. Less important than the others.

The exact weighting can shift depending on your profile, and your score updates constantly. You can't isolate any single action and say "this raised my score by exactly X points." But the categories tell you what lenders actually care about, and where to focus. For a deeper breakdown of each category, myFICO's guide is a solid resource.

Why credit matters (even if you hate the idea of debt)

A lot of people assume credit only matters if you want to borrow money. That's not quite right. Your credit affects:

- Renting an apartment. Most landlords run a credit check as part of the application.

- Car loans and mortgages. Your score determines whether you qualify and how much interest you'll pay. On a 30-year mortgage, the gap between "good credit" and "okay credit" can add up to tens of thousands of dollars.

- Phone plans and utilities. Some providers require a deposit if your credit is thin.

- Certain jobs. Especially in finance, government, and roles with financial responsibility.

- Insurance rates. In most states, insurers can use credit-based scores to set premiums.

Even if you never plan to take on major debt, your credit affects the prices and options available to you. Building history early puts you in a stronger position later.

Starting from zero

If you don't have any credit history, you're in what's sometimes called a "credit invisible" situation. It's a chicken-and-egg problem: you need credit to get credit. But there are a few ways in.

Most people start with one of three options: a traditional starter card (often hard to get approved for without prior history), a secured card (which requires an upfront deposit), or a card like Atlas¹ that reports to all three bureaus2 with no hard credit pull and no deposit required.

Whichever route you take, a few habits matter more than anything else:

- Pay every bill on time. Payment history is 35% of your score. Autopay is your friend.

- Keep utilization low. Try to stay under 30% of your credit limit. Under 10% is even better.

- Don't apply for new credit constantly. One hard inquiry every few months won't hurt. Five in one month will.

- Let time do its work. Length of history is a factor you can't rush. The sooner you start, the more you have working for you later.

The bottom line

Credit is a long game. It rewards consistency more than any single big move. You don't need to obsess over your score, but ignoring it for a decade can cost you real money and real options when you finally need them.

Understanding how credit works really comes down to a handful of habits: start earlier than you think you should, pay on time, and keep balances reasonable. That's most of it.

Frequently asked questions

How long does it take to build credit from scratch?

You can typically generate a FICO score after about six months of credit activity. Building a strong profile takes longer, usually several years of on-time payments, low utilization, and accounts aging. The good news: once you start, time does most of the work for you.

Does checking my own credit score hurt it?

No. Checking your own credit is a soft inquiry, and soft inquiries don't affect your score. Feel free to check as often as you want. Plenty of free tools let you do it without any impact.

What's a good credit score?

FICO breaks scores into tiers: 300–579 is the lowest range, 580–669 is fair, 670–739 is good, 740–799 is very good, and 800–850 is exceptional. Most lenders reserve their best interest rates for scores in the mid-700s and up.

Can I build credit without a credit card?

Yes. A few options: becoming an authorized user on someone else's card (their history shows up on your report), rent reporting services that turn on-time rent into credit history, and tools like Experian Boost that give you credit for on-time utility and phone bill payments.

Will closing a credit card hurt my score?

It can. Closing a card reduces your total available credit, which bumps up your utilization ratio. It can also shorten your average account age if the card is old. Usually the impact is minor, but closing your oldest card or one with a high limit can sting more than you'd expect.

¹ 0% APR. The Atlas Card is issued by Patriot Bank N.A. and Academy Bank N.A., Members FDIC and pursuant to a license from Mastercard. Atlas program terms apply. See atlasfin.com/policies for details.

2 Improvement in your credit profile is dependent on your specific situation and financial behavior.

Apply In Minutes

• Just takes two minutes to apply 3

• 0% APR with limits that grow with you

• No credit history needed

By clicking "Get Started" you opt-in to receive account and marketing messages at the entered number and agree to Atlas' terms of service, mobile terms and privacy policy. Message frequency varies. Message and data rates may apply. You can opt-out at any time by replying STOP, or text HELP for support.

.jpg)

.jpg)